Markets have undergone a paradigm shift and have migrated in just a few years from operations carried out entirely by people in person to fully electronic operations thanks to technological advances. This has contributed to the appearance of new players within the investment world, new ways of trading, and even new markets.

Undoubtedly, all this has caused a democratization of investing, allowing access to retail traders who were barred from participation not so many years ago.

Transformation of Markets

Markets have migrated from in-person operations carried out by people to completely electronic systems. This technological change has brought with it new players, innovative operating methods, and alternative markets.

Uncomfortable Reality

It's no coincidence that most retail traders lose. The entire industry is set up for this to happen, and their participation simply serves as another (very small) source of liquidity provision to the market.

It's important to keep your feet on the ground. The world of trading and investing is too complex for a retail trader from home, with an internet connection and a computer, to obtain any return on their capital. Everything is stacked against them.

Competitive Context

Modern trading is dominated by large institutions that dedicate enormous amounts of money to developing powerful tools and hiring the most skilled people. The independent trader has a significant competitive disadvantage.

Knowing those who have the capacity to influence price movement offers us a more solid viewpoint when making trading and investment decisions. Financial markets are composed of various agents with different ways of operating based on their needs at that specific moment.

"One of the biggest mistakes we can make is thinking that all market movements are orchestrated by a single entity; or distinguishing traders between professionals and non-professionals in a simplistic way."

- Ruben Villahermosa

When terms like "strong hands" and "weak hands" are used, it's from the perspective of understanding who has greater market control, not with the objective of seeing it as a war between institutions and retail traders since, in the most traded assets, retail traders have little or nothing to do with it.

Keep in mind that everything also depends on the volume traded in each particular asset. As that volume increases, greater intervention will come from large participants.

For example, the American S&P 500 index is practically entirely controlled by large institutions, where 90% or more of the volume comes from them. It's a battle between them. No trade can be executed without an institution willing to take one side of the position and another institution willing to take the opposite side. The market cannot move the slightest tick if there isn't an institution behind every movement.

On the contrary, assets that move very little volume can be influenced by operators with less capacity. That's why trading assets with low liquidity is generally not recommended, to avoid possible manipulations.

Our objective is therefore to analyze chart behavior to try to determine which side most of the institutional money is on.

Types of Participants

Let's categorize the different market participants according to their intention:

Video in Spanish with English subtitles available

Video in Spanish with English subtitles available

Hedging

Definition

Basically, it involves executing financial operations aimed at canceling or reducing risk. They consist of acquiring or selling a product that is correlated with the asset on which coverage is to be established.

While it's true that the main objective of hedging is to limit risk, it can also be used to secure a latent profit or preserve the value of a fixed asset. These operators don't care about the direction price takes since it's not their company's main business. They don't trade with directional intent and have a longer-term view.

Examples of traditional producer-oriented hedging:

- An airline company that buys oil futures as a resource to balance their fuel costs

- An international import and export company that acquires currencies to hedge against possible price changes

Market makers would also be included in this category since they could come to the market depending on their needs with the objective of maintaining a neutral risk of their total positions.

Speculation

Unlike hedging operators, who basically trade to reduce their risk exposure, speculative traders assume risk when opening their positions.

If given current market conditions they consider the asset's price to be cheap, they will buy, and vice versa if they consider it expensive, with the sole objective of profiting from price movement.

Speculative Participants Include

- Hedge funds with diverse strategies

- Investment funds seeking returns

- Proprietary trading firms

- Institutions operating through high-frequency algorithms

They are the most active operators in the financial market. They basically focus on searching for liquidity zones since due to the large amount of volume they move, they need that counterparty to match their orders.

Common Mistake

There's a very common mistake in thinking that all institutions are profitable. Many of those institutions are the preferred victims in the financial market since they move significant amounts of volume and possibly have a weak operational approach.

Although they don't have a purely speculative character, some options traders could be included in this category since if they have a large position open in the options market, they're very likely to also come to the futures market to try to defend it if necessary.

Arbitrage

It consists of taking advantage of financial market imperfections. These operators observe a price inefficiency and execute transactions with the objective of correcting it and adjusting prices.

Trading a Single Product

Taking advantage of temporary inefficiencies in the same asset.

Correlated Products

Trading different products that should move together.

Between Different Markets

Such as the spot market and futures (e.g., EURUSD vs 6E).

Between Contracts

Trading contracts with same and different expiration.

Practical Example

We can have the euro-dollar currency pair (EURUSD) and the derivative in the futures market (6E). An arbitrage strategy will take advantage of the minuscule price difference that may exist between these two markets to obtain an economic profit.

Central Banks

Separate from the previous ones, we also have Central Banks. They have the greatest capacity since they direct the monetary policies of countries primarily through the establishment of interest rates.

Of the types seen, the only one that would enter the market with the directional objective of adding pressure to one side or the other would be the speculative operator. The rest of the transactions would have other intentions but would equally be represented ultimately on the price.

The fact that not all trading is speculative in nature is a very important factor to consider. Many make the mistake of thinking that each negotiation has directional interest behind it, and in most cases, this is not so. There are many types of participants interacting in the market, and each one's needs are different.

In addition to trading intent, it's worth noting the different use of timeframes that different operators work with. While some take the shortest term into account, others maintain medium or long-term strategies. The key point is that each and every market movement is being supported by a large institution and that at any moment another one may enter with a longer-term perspective and greater capacity to influence price.

Electronic Markets

Since 2007, exchanges have gone from being controlled by humans to a fully automated and electronic environment where really the only thing present are computers responsible for performing order matching processing.

With the arrival of new technologies, computational advances, and regulatory changes to the financial world, the importance of speed in transmitting and receiving data has grown more and more, reaching the current moment where electronic trading represents most of the traded volume.

Degree of Electronification

| Product | Electronification |

|---|---|

| Futures | 90% |

| Stocks | 80% |

| CDS on Indices | 80% |

| Corporate Bonds | 25-40% |

Corporate bonds are at the lower end of the spectrum since they are more customized products.

Benefits of Electronification

All these advances have allowed perfecting market efficiency by adding liquidity, reducing costs, increasing execution speed, improving risk management, and allowing access to specific markets.

Algorithmic Trading

Definition

It is an order execution process based on well-defined and coded rules carried out by a computer automatically, thus avoiding human participation. It employs complex statistical and econometric models on advanced platforms to make decisions electronically and independently.

It mainly uses price, time, and volume as variables; and was developed to take advantage of the speed and data processing advantages that computers have over human operators.

These strategies interpret market signals and implement trading strategies automatically based on them, with operations of varying duration.

The increase in market share in recent years of algorithmic trading in all types of assets is simply spectacular, and forecasts for subsequent years follow the same dynamic. One of the reasons for such growth is due to the emergence of artificial intelligence in the financial sector.

High Frequency Trading (HFT)

High Frequency Trading is a type of algorithmic trading but applied at the microsecond scale, trying to profit from very small changes in asset prices.

It's based on the use of mathematical algorithms with which orders are analyzed and executed based on market conditions. They perform thousands of operations in a short period of time, managing to make money systematically and with high probability.

Their main advantage is processing and execution speed, which they achieve thanks to the dedication of powerful computers. That's why the general public trading from home simply doesn't have the means to access this type of trading. Therefore, it's a style reserved almost exclusively for institutional operators with significant capital.

Although in Europe it's slightly lower, the share in the American stock market continuously represents about 50% of the total traded volume. It's interesting to note how the 2009 crisis caused a decrease in HFT participation mainly due to increased competitiveness, high costs, and low volatility.

Don't Confuse

Don't confuse High Frequency Trading with automated systems that a retail trader can create (which can fall into the algorithmic trading category). Generally, these types of tools (known as EAs, robots, or bots) are usually not very effective; quite different from HFT, which costs millions of dollars and has been developed by large financial firms.

How Do High-Frequency Algorithms Affect Us?

The fact that in current markets most of the traded volume comes from high-frequency algorithms doesn't greatly influence structure-based analysis that we can do, mainly because we're not competing to exploit the same anomalies.

The Advantage of Wyckoff Analysis

While our analysis seeks to take advantage of a deterministic aspect of the market where we try to discern who has greater control (buyers or sellers), high-frequency algorithms seem to be located more in the random aspect of it: arbitrage, momentum directional strategies and event-based strategies, and market making.

While it's true that some algorithms may execute directional strategies, these cover the shortest term, and although they could distort our analysis, the advantage that studying the Wyckoff methodology offers us is that it provides a structural framework thanks to which we can minimize part of the noise that originates in the smallest scales and obtain a more objective sentiment of current market conditions considering a larger context than what these algorithms cover.

OTC Markets

It's a type of electronic market where financial assets are traded between two parties without the control and supervision of a regulator, as happens in stock exchanges and futures markets.

Difference Between Centralized and OTC Markets

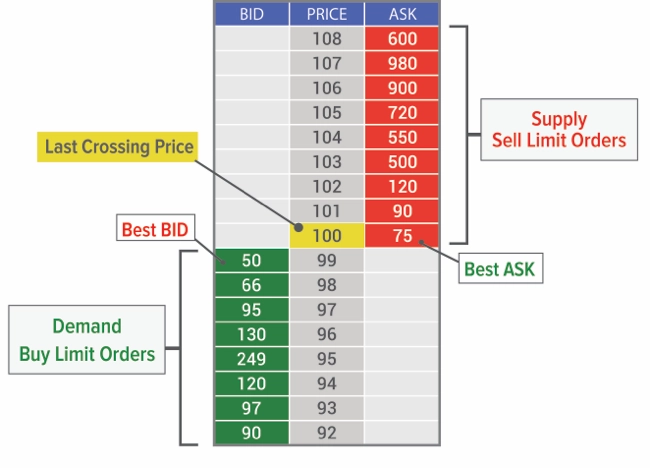

Centralized (On-Exchange)

There is a single order book which is responsible for linking all participants in that market. Greater transparency.

Non-Centralized (Off-Exchange/OTC)

There are multiple order books (as many as there are market makers) where the lack of transparency becomes evident by only showing the BID and ASK price.

Market Fragmentation

In recent years, the American market has undergone a fragmentation process where more and more decentralized markets have been created. Currently, US stock liquidity is divided among approximately 88 different sources, with almost 40% of trades being carried out in non-centralized markets.

Types of Brokers

Within non-centralized markets, we find different brokers based on how they handle their clients' orders:

With Dealing Desk (Market Makers): They act as the client's counterparty. By having the ability to take the counterparty in operations, the door opens to possible conflicts of interest: if the client wins, the broker loses and vice versa.

Without Dealing Desk (Non Dealing Desk): They act as intermediaries between the client and the rest of the market. This is who you should work with since they offer a more transparent process.

Danger for the Retail Trader

When the fact that the market owner is responsible for offering the final price is combined with the possibility that they are at the same time the counterparty, the retail trader is exposed to suffering some type of price movement manipulation.

It's also important to know that, by the very nature of this type of non-centralized market, there can be different prices for the same asset. That is, if we want to trade the EUR/USD currency pair, each market maker will offer us a different price and volume.

How Do OTC Markets Affect Us?

The Data Problem

The analysis we do under this type of market will be based on data that, although it could be a significant representation of the market, doesn't really genuinely represent all price and volume data.

To have this data faithfully, we must analyze said asset under a centralized market. For example, for EUR/USD we must analyze the futures market (centralized market) which corresponds to the ticker $6E.

Practical Solution

If you don't have enough capital to trade futures, you can analyze the asset in the futures market and execute trades through a CFD with a good broker (that's not a market maker). An intermediate option is to trade the micro future, which in the case of EURUSD corresponds to the ticker $M6E.

If you open a chart of the future (6E) and the CFD (EURUSD), you'll see that price movements are practically identical even though they are different markets. This is possible thanks to an arbitrage process carried out by high-frequency algorithms that occurs systematically between both markets.

Dark Pools

What Are They?

Definition

A Dark Pool is a private market (Off-Exchange) that connects institutional investors and facilitates the exchange of financial assets with the peculiarity that their transactions are not reported immediately, with the traded quantity (volume) unknown until the following 24 hours.

Market Share

- Trading in non-centralized US stock markets is approximately 35%, with 16 to 18% being executed in Dark Pools

- According to a Bloomberg study, Dark Pool trading together already represents about 30% of total traded volume

- In Europe, the share has expanded rapidly: from 1% in 2009 to 8% in 2016

Why Do They Exist?

When a large institution wants to buy or sell a huge amount of an asset, it goes to this type of market for several reasons:

- They know that if they access the public market, it will cost them to find counterparty

- They would possibly get a worse price in the open market

- They would be exposed to predatory techniques like Front Running executed by HFT

- They get better commissions by saving on fees required by public markets

Dark Pool Regulation

Important Information

Contrary to what many people may think, Dark Pools are highly regulated since their owners are registered with the SEC (Securities and Exchange Commission) and FINRA (The Financial Industry Regulatory Authority), therefore they are subject to regular audits and examinations similar to those of a public market.

In addition to private financial institutions, there are public exchanges that have their own Dark Pools like the New York Stock Exchange (NYSE), the most traded and most liquid exchange in the world.

The CME (Chicago Mercantile Exchange), which is the market with the largest number of options and futures contracts in the world, also has its own Dark Pool and offers this opaque trading service through what they have called "Block Trades".

"A Block Trade is a privately negotiated futures, options, or combination transaction that is permitted to be executed apart from the public auction market. Participation in Block Trades is restricted to eligible contract participants. Block Trades may be executed at any time at a fair and reasonable price."

- CME Group

How Do Dark Pools Affect Us?

Activity carried out in Dark Pools plays an important role in determining intraday returns and in the uncertainty that can be related to them, therefore having important microstructural implications.

Implication for Analysis

We may be analyzing an asset in which very significant transactions may have occurred in a hidden manner, and obviously, we cannot even assess the buyer's intentions.

These transactions, by not being determined by public market supply and demand, don't have an immediate impact on price formation. However, there are studies that claim that public market operators react to the report of orders executed in the Dark Pool once it is released, potentially significantly altering the analysis of interaction up to that point.

Randomness vs Determinism

This issue is another of the great debates within the trading community and undoubtedly generates great controversy. The vast majority who side with market randomness do so with the aim of discrediting the usefulness of technical analysis. On the other hand, we have those who observe each and every price movement and attribute an intention to it, a grave error. Not everything is black or white.

The Two Perspectives

Random Perspective (Efficient Market Hypothesis - EMH): The current price already reflects all information from past events and even from events that the market expects to take place in the future. That is, all information about the asset is absolutely discounted and therefore it's not possible to predict future price action.

Deterministic Perspective: Price movements are influenced by external factors, so knowing what those factors are, future price action can be predicted and therefore it's possible to obtain a profit from market interpretation.

When speaking of randomness, it refers to that market movement having no logical intention behind it; it's simply a price fluctuation. Randomness is born as a result of the innumerable variables that take place in the market. Nobody can know how the rest of the market participants will act. If someone knew, they would have a deterministic system whose predictions would be correct 100% of the time.

Logical Conclusion

Market Reality

If the Efficient Market Hypothesis (EMH) and market randomness were valid, nobody could obtain gains consistently. And it has already been demonstrated throughout history that this is not the case. On the other hand, markets also cannot be modeled as a completely deterministic process where there is no randomness, since this would mean there would be strategies with a 100% probability of success, and this is also not the case.

We therefore arrive at the conclusion that financial markets are composed of a percentage of randomness and another deterministic percentage, without being able to determine how much weight each one has.

The Adaptive Markets Hypothesis (AMH)

This theory would be supported by the Adaptive Markets Hypothesis (AMH) presented by American financial economist Andrew W. Lo in his book "Adaptive Markets" (2017), which shows market efficiency not as a present or absent characteristic, but as a quality that varies according to market conditions.

- Market efficiency depends on its conditions. This changing characteristic is the result of participant interactions which in turn depend on market conditions

- The agent is not totally rational and is subject to cognitive biases. A purely rational model cannot be applied since participants form expectations based on different factors. With the same information, different expectations can be created

- Each agent has different degrees of risk aversion that influence their decisions

Although the author refers to agents as individual people, this is equally applicable to the current trading ecosystem where we have already mentioned that practically all actions are done by algorithms electronically. This fact doesn't modify the base of the adaptive hypothesis since, regardless of the market participant and the way they interact with the rest of the market, they will make their decisions based on the valuations, motives, or needs they have at a given moment; and that given moment will be conditioned by different factors that will change over time.

Rationality and Irrationality Coexist

The AMH doesn't focus on discrediting the Efficient Market Hypothesis, it simply treats it as incomplete. It places more value on changing market conditions and how participants can react to them. In the market, rationality and irrationality can coexist at the same time (efficiency and inefficiency) depending on conditions.

Where Does the Wyckoff Methodology Fit?

Landing it on what concerns us, market reading under the principles of the Wyckoff methodology is based on a deterministic market event: The Law of Cause and Effect. For the market to develop an effect (trend), a cause must first occur (accumulation/distribution). There are other deterministic events that can offer an advantage, such as seasonality.

An example of random behavior could be seen in High Frequency Algorithms. We have already mentioned some of their uses and they are the perfect example of forces that have the capacity to move the market and don't necessarily have directional logic behind them.

Finally, it should be noted that most studies defending market randomness use classic chart patterns (triangles, head and shoulders, flags, etc.) or some price pattern without underlying logic behind them to confirm the lack of predictability of technical analysis in general. Our approach to trading markets is very far from all this.

"There are studies where using an analytical tool as simple as trend lines, non-random behavior in financial markets has been evidenced, even being able to exploit an anomaly to obtain certain returns."

- Ruben Villahermosa

Wyckoff 2.0: Structures, Volume Profile and Order Flow

This article is an excerpt from the book. In it you will learn advanced knowledge about today's trading ecosystem, the different participants and their interests, the nature of OTC markets, what Dark Pools are, and professional tools like Volume Profile and Order Flow. You'll be able to see the supporting charts that accompany the article and much more!

View book